SpaceX, Adding It Up: What the Compute Contracts Commit

A contract reported as $30 billion, and what, under its own terms, it actually commits.

Yesterday’s piece counted the cash SpaceX has disclosed it must spend, against what the offering raises. This one is narrower. A contract was filed the morning that piece ran, reported as $30 billion of revenue. Read for what its own terms require, that number is smaller, and it arrives later than the cash that has to go out to earn it. The subject here is timing: when the money moves, and which way.

The announcement

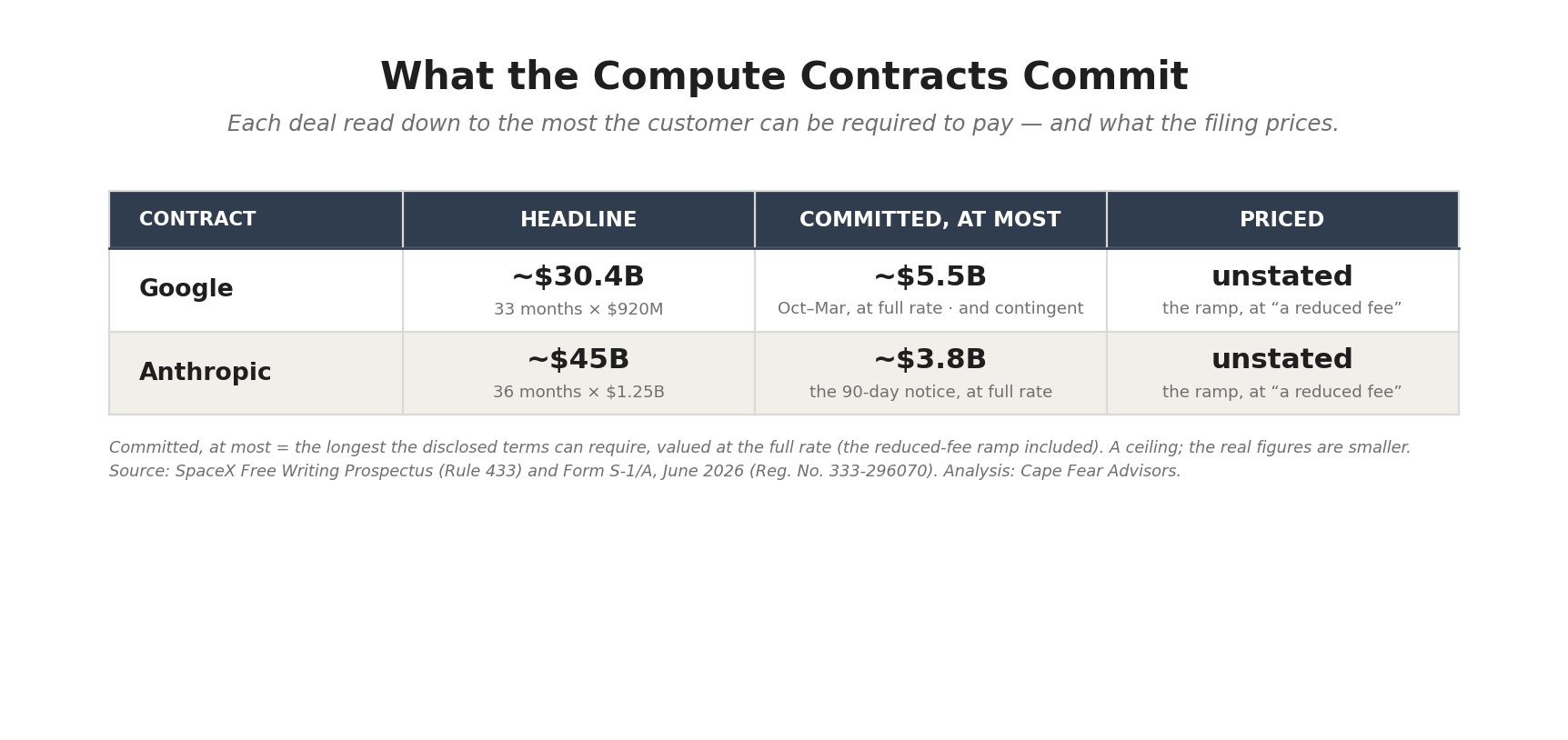

On June 5, 2026, SpaceX filed a free writing prospectus, a Rule 433 supplement to its IPO registration statement, disclosing a Cloud Service Agreement signed that day with Google LLC. In the filing’s words, Google “agreed to pay us $920 million per month from October 2026 through June 2029” for access to roughly 110,000 NVIDIA GPUs and supporting infrastructure, about $30.4 billion across the 33-month term. Capacity ramps through September “at a reduced fee.” If SpaceX fails to deliver the committed GPUs by September 30, 2026, then after a one-month grace period Google may terminate, or take fewer chips at a pro-rata-reduced fee. After December 31, 2026, either party may terminate on 90 days’ notice.

It is the second contract of this shape. On May 3, SpaceX signed cloud services agreements with Anthropic: $1.25 billion per month through May 2029, capacity ramping in May and June “at a reduced fee,” terminable by either party on 90 days’ notice, for roughly 325,000 GPUs across Colossus and Colossus II.

The actual commitment

Both contracts headline large. Each thins at every step when read through three figures: the full-term total, the part the customer cannot cancel, and the part the filing actually prices.

The cancellation terms set the ceiling, so take the most the disclosed terms can require, valued at the full rate. Google cannot terminate until after December 31, 2026, so the most it owes is October through the 90-day notice period that follows: about six months, roughly $5.5 billion, and even that is contingent on SpaceX standing up 110,000 GPUs by September 30. Before delivery, it is zero. Anthropic, terminable by either party on 90 days’ notice from signing, owes at most the notice period: about three months, or $3.8 billion if the reduced-fee ramp is counted at the full rate. These are generous ceilings. The real figures sit below them.

The term is the filing’s: terminable by either party on 90 days’ notice. The controlling shareholder has supplied the reason for it, in public. On May 28, Elon Musk wrote that “SpaceX has not committed to leasing Colossus for years,” that the short term “was our request, not Anthropic’s,” and that “if compute gets super tight,” SpaceX “might need it back.” The out reads less as a concession to the customer than as the company keeping capacity it may need for itself. The conditionality runs in both directions at once. The revenue depends on building the capacity, and the commitment depends on not needing it back.

And the firm windows are the ramp months, priced in both contracts at “a reduced fee” with no amount and no floor stated. The full monthly rates, $920 million and $1.25 billion, describe the periods after the ramp, which the customer may never reach. The committed period is the period the filings decline to price.

So of roughly $75 billion in combined headline, the most the disclosed terms can require is about $9 billion: both notice periods, valued at the full rate, with SpaceX delivering. That is the ceiling, and the real figures sit below it. A fraction of the headline, either way.

The cash call

What the contracts do commit SpaceX to is the build. And the build comes first.

The filing states one hard capacity figure: Colossus and Colossus II “collectively provide approximately 1.0 gigawatt of compute power,” reached in the first quarter of 2026. The two contracts call for roughly 435,000 GPUs across those facilities, and xAI trains its own models on the same hardware. If the existing gigawatt is largely committed, much of it to Anthropic and the rest to xAI’s own training, then Google’s 110,000 GPUs are new capacity. If some of it is free, the new build is smaller. Either way, the capacity has to exist, and be running, by September 30.

The cost of it is in the company’s own numbers. The AI segment spent $12.7 billion of capital expenditure in 2025 and $7.7 billion in the first quarter of 2026, roughly $20 billion to stand up about a gigawatt. Give the company every benefit on the economics: call the per-gigawatt cost lower than that, assume it falls with scale. None of that is the argument here. The argument is only how much has to be spent, and when.

Even at a discount, Google’s 110,000 GPUs — about a fifth of a gigawatt — are several billion dollars of capital, and the deadline is September 30. It is June. The spend goes out this quarter and next, on top of the $7.7 billion the AI segment already laid out in the first quarter, to bring a new cluster of power and cooling online inside four months. The company says, in the prospectus, that it brought a Colossus II cluster online in 91 days. From June, 91 days reaches September, at the edge of the date.

That is the sequence the contract sets. The capital goes out now, this quarter, to build capacity that earns a monthly fee beginning in October, at a reduced rate through the ramp, under an agreement the customer can leave after December. The cash leads the revenue by the full cost of the build, and the revenue at the end of it is cancellable and, where firm, unpriced.

What it adds to

Yesterday’s piece found a cash requirement the offering does not meet, disclosed but not sized, and expected the largest of it to land in the near term, ahead of revenue. The contracts are consistent with exactly that. Dated to a September delivery and an October start, they put a name and a date on the near-term spend the cash analysis anticipated.

They do not, on their own, enlarge the gap, and we do not claim they do. They sharpen its timing. The build precedes the revenue, the revenue is mostly optional, and where the cash comes from is the question the last piece left open. Nothing filed this week has closed it.

A note on value

These contracts have also been read as a verdict on the company’s worth: proof, in some accounts, that the cash question is now answered. Settling the valuation is not this piece’s purpose, and it does not try. But the question earns a note, because the leading public valuation of SpaceX rests, at one point, on the financing question these contracts make concrete.

Aswath Damodaran’s post-prospectus valuation is a well-considered and excellent model, the most transparent public assessment of the company, every input visible, the spreadsheet posted for anyone to download and change. It is the work we would send a reader to first. On his own numbers he arrives at $1.25 to $1.35 trillion of equity value, and he notes that the offering price stands at 138% of it.

He asked his readers to do one thing, and we did it. “Listen,” he wrote of the sales pitches to come, “but check the numbers for plausibility and make your own judgments.” So we checked one. His model carries an explicit input: a probability of failure of zero. For a company that burns cash and needs capital well beyond the offering, a zero is a strong number, the kind worth confirming before it is relied on.

The documents say the same thing, in their own register. The prospectus describes this company’s funding in the conditional throughout: liquidity “sufficient for at least the next twelve months,” an intention that it “may issue a significant amount of equity,” funding that “depends on continued access to the capital markets,” and the compute contracts themselves, terminable on notice and contingent on a delivery the company “may fail” to make. That is the language of a risk to be confirmed before it is assumed away.

We note only what was asked, and what we found: an excellent model rests, at this one input, on a zero, and the filing that supplies its other inputs describes the same risk in “may.”