SpaceX, Adding It Up: The Record-Breaking IPO Week

The announcements increased pressure on cash, and left the gap unresolved

On June 12, the world’s largest IPO launched. SpaceX became a publicly held company at a valuation near $1.8 trillion. Throughout the week, SpaceX emphasized, formally and repeatedly, the importance of the Terafab project and its intention to pursue it, nearly as a matter of necessity. At the same time, the documents underscored how conditional the potential cash sources for the project remain, and stayed silent on the scale. The picture is now tighter on the need, and leaves open the question: whence the cash?

The mechanics ran on schedule. The registration statement was declared effective on the morning of June 11. The company priced at a fixed $135 per share — no range, no book-built discovery — and filed its final prospectus the morning of the trade. On June 12, SpaceX began trading on Nasdaq under SPCX, opening sharply above the offering price and taking its place among the largest public companies in the world by market value. With the underwriters’ option exercised, the offering raised approximately $86 billion. By every market measure, the largest public offering in history succeeded.

On June 8, in a recorded conversation with Jamie Dimon filed with the SEC as a free-writing prospectus, Elon Musk was asked what compelled him to build chip fabs now, alongside everything else he was doing. His answer placed Terafab at the center. He described the limiting factor as the ability to make chips — logic, memory, and packaging — and said there is not a single high-volume computer memory fab operating in America, that the nearest, Micron’s in Idaho, will not reach volume production until 2028, and that even the best-case assumptions of existing manufacturers fall short of anticipated demand. His conclusion: “that’s why we need to do Terra Fab. It seems essential. Otherwise... there will not be enough chips.” In the registration statement, Terafab had been a collaboration the company was under no obligation to complete. Three days before the offering, the company’s controlling shareholder called it essential.

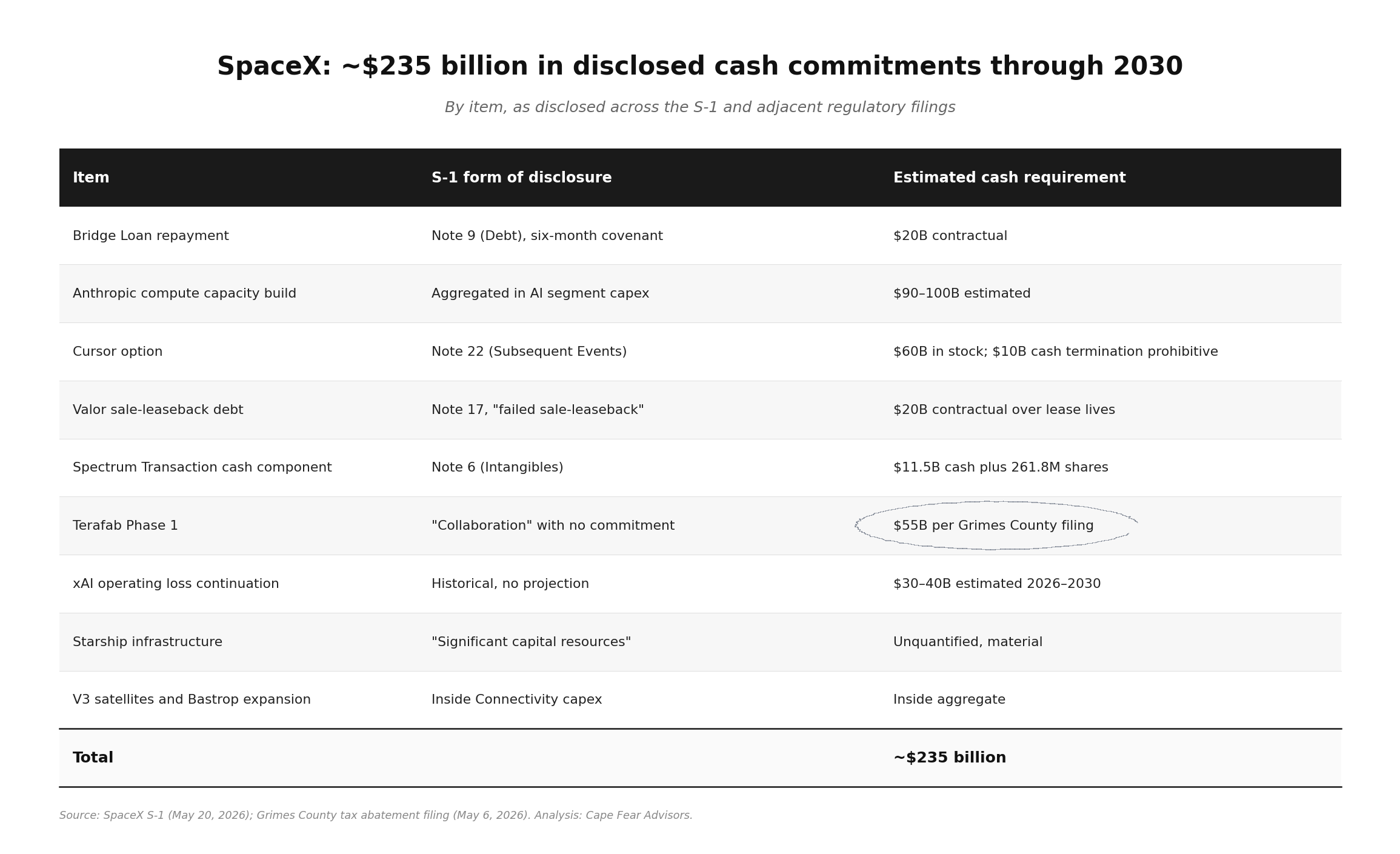

Figure unchanged from “The $235 Billion Cash Gap” (May 21, 2026). In the filings, the Terafab line was a collaboration with no commitment. On June 8, the company described it as essential.

On funding, the same filings stayed at the level of intention. The company wrote that it “plan[s] to access a range of debt and equity financing solutions available to us as a public company to fund future investments in growth,” and that its capital expenditures “will scale as quickly as we are able to deploy power and compute.” The requirement itself was never quantified. The tax-abatement filing the company submitted to Grimes County in May had placed Terafab’s first phase at $55 billion — the figure carried in the table above — while the offering documents named no Terafab commitment at all. And in the same disclosure that carried the necessity, the company set down its conditions: “while we expect to construct Terafab to address such supply constraints, Terafab may not be successful,” it “may not be able to achieve our objectives with respect to Terafab within the expected timeframes, or at all,” and “neither Tesla nor Intel are obligated to remain a part of the project, and we may not enter into any such definitive agreements.”

That is where the week leaves it. The opportunity to raise cash came and went, with a clear success: the offering priced, traded, and closed among the world’s most valuable companies. In the same days, the company moved Terafab from a collaboration it was not obligated to complete to a project its controlling shareholder called essential — while the documents that would fund it named no commitment, quantified no requirement, and conceded the project may not proceed at all. The need is arriving sooner than it was a week ago. The sources are no nearer. The question that opened the week is the question that closes it: whence the cash?