SpaceX, Adding It Up: The Probability of Failure

Professor Damodaran asked his readers to check the numbers. We checked the one left at zero.

The leading public valuation of SpaceX is also the most transparent. Its author posted the spreadsheet, made every input visible, and told readers to check the numbers for plausibility and reach their own judgments. The earlier notes in this series checked the cash the company has disclosed it must spend. This one is narrower. It checks a single input, the probability of failure, against prior models, and against the public filing.

The input

In Professor Damodaran’s framework, the probability of failure is a standard input: the chance, over the foreseeable future, that the company does not survive as a going concern, applied as a haircut to the computed value. The model leaves it switched off unless the user turns it on. In his SpaceX valuation, in April and again in June, it is off, at the model’s default of zero. In the same block of inputs he turned on the two assumptions directly above it, the cost of capital and the return on capital after year ten, and entered bespoke values. The failure input stayed at the model’s default, which states the assumption in the model’s own words: no chance of failure over the foreseeable future.

What earns a zero

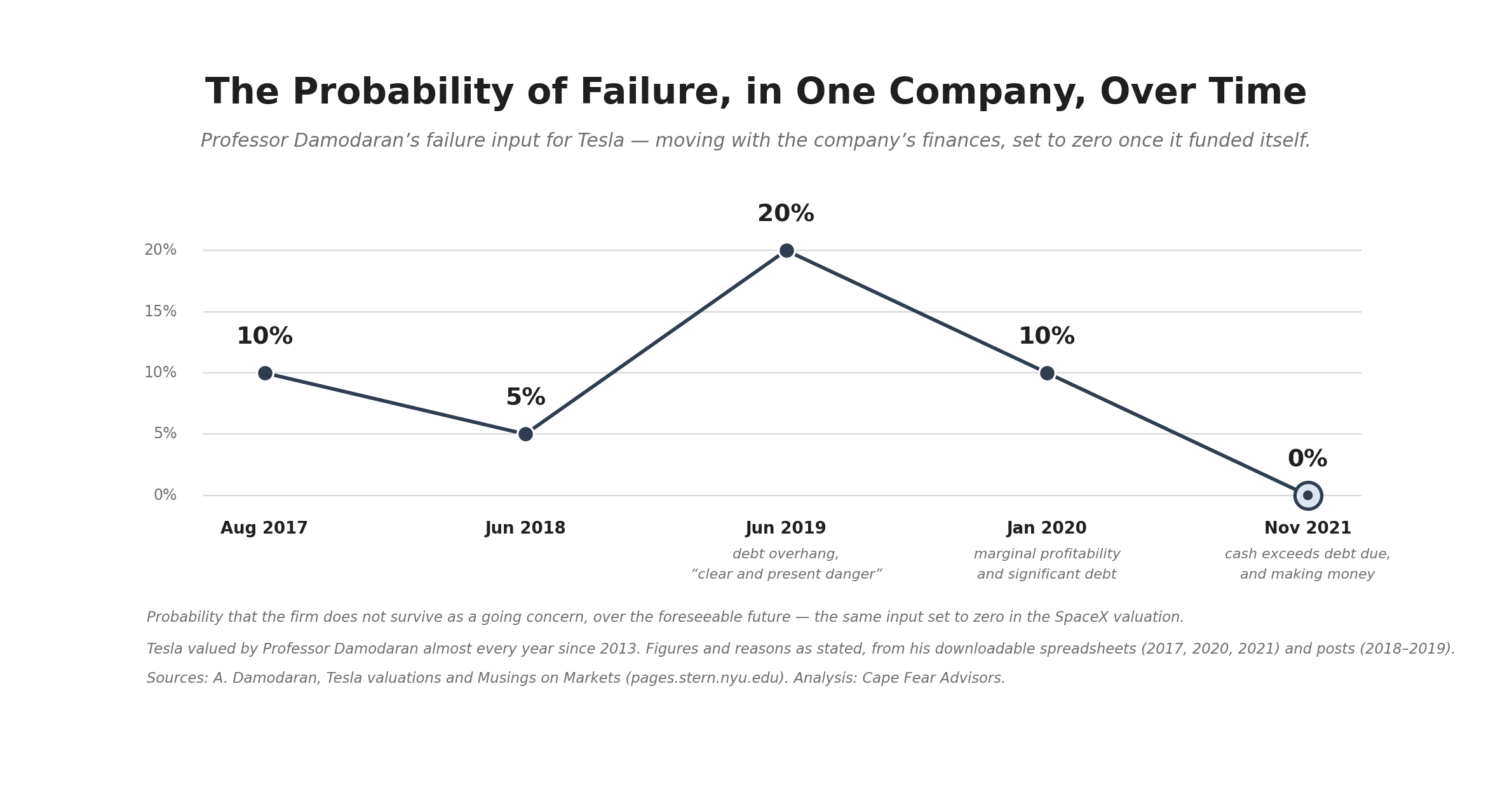

Professor Damodaran has switched that input on before, and moved it, for a single company over time. He first valued Tesla in 2013 and has valued it almost every year since, and the failure probability tracked the company’s finances.

In June 2019, with a debt overhang he called “a clear and present danger” and a real chance of the company losing access to new capital, the probability of failure was set to 20 percent. As Tesla steadied it dropped, to 10 percent in early 2020, and in November 2021, once the company had, in his words, “a cash balance that exceeds its debt due and is making money,” he set it to zero. The zero was not where he began. It was reached, once the company funded itself.

The companies that carried a number

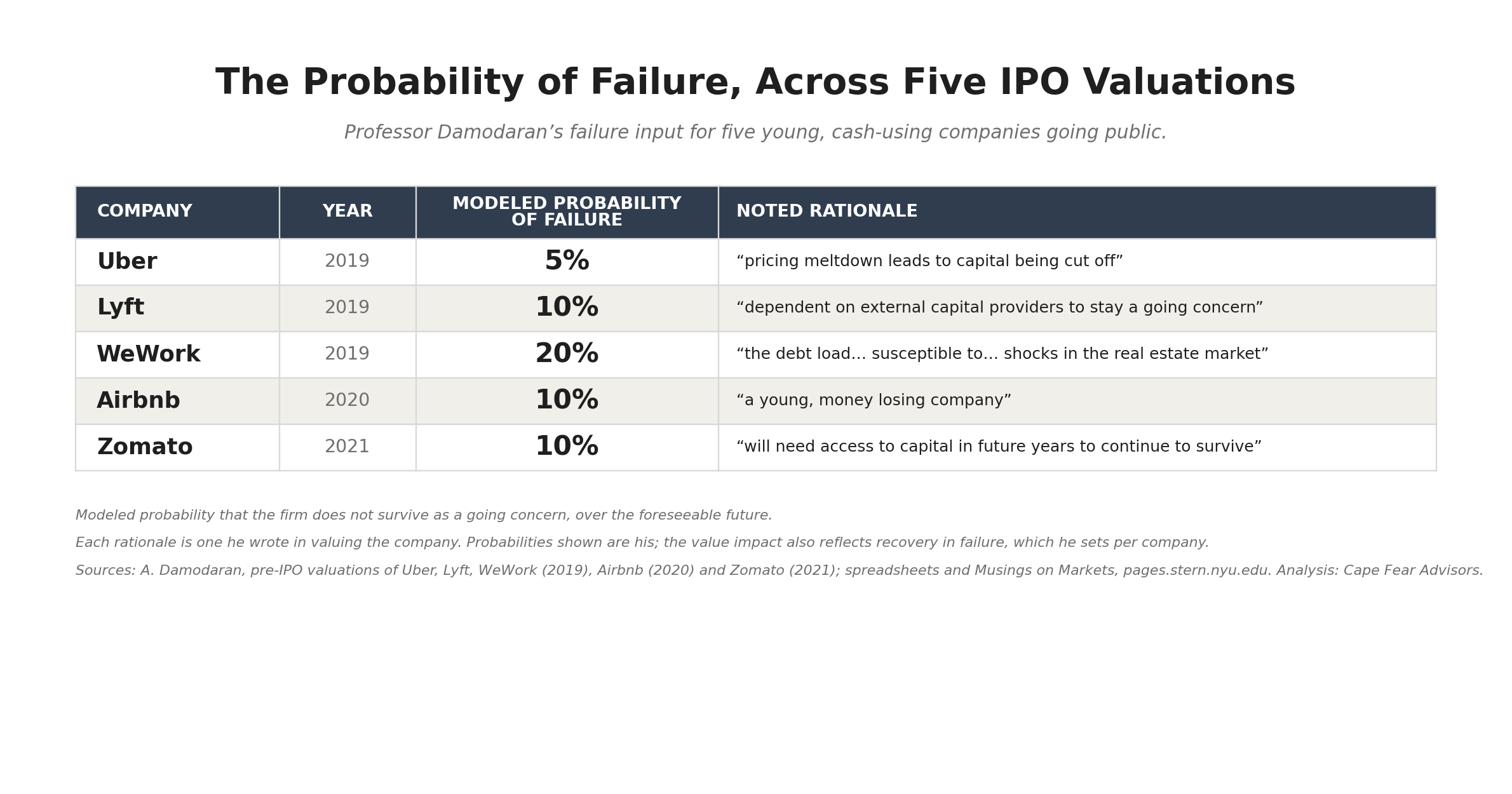

The same input, set for companies at the stage SpaceX is at now, young and raising money in public markets, has never been zero.

In his pre-IPO valuations he assigned Uber 5 percent, Lyft 10, WeWork 20, Airbnb 10, and Zomato 10. The reasons he wrote beside them turn on the same thing: Lyft “dependent on external capital providers to stay a going concern”; Uber a pricing collapse that “leads to capital being cut off”; WeWork a debt load that leaves it exposed to “shocks in the real estate market.” Two of these sit closest to SpaceX. Airbnb was the soundest of the group: near profitability, little debt, a known brand. It still drew 10 percent, because it remained “a young, money losing company.” Zomato held a large cash balance, larger after its IPO, and still drew 10 percent; the cash pushed down the risk, he wrote, but the company “will need access to capital in future years to continue to survive.” A strong position did not earn a zero in his hands, and neither did cash on the balance sheet. Self-funding did.

Where the filing puts SpaceX

In the observed practice, the probability falls to zero once a company funds itself. The filing says SpaceX has not reached that point. It states that its access to the capital markets or other financing “may be adversely affected by factors beyond our control,” that it “may issue a significant amount of equity,” and that its liquidity is sufficient “for at least the next twelve months.” By the measures used in prior valuations — young, raising, dependent on outside capital — SpaceX sits with the companies that carried a number. This particular valuation carries zero.

Adding it up

The zero reaches most of the resulting valuation. More than four-fifths of the value lies beyond the ten-year forecast, in the terminal value, and the company has to survive the whole way to collect it. The cash requirement runs the other direction: near-term, inside the forecast, the commitments the earlier notes totaled against the raise. So the shape of it is a near-term reliance on raising capital, crossed in order to reach a value that is almost entirely back-loaded, with the one input that would price the survival risk left at zero. In the settings, where a failure costs half of fair value and is applied once, each percentage point of failure probability would subtract about $6.1 billion from the value of its operating assets. At zero it subtracts nothing, and the half recovery it would soften never comes into play.

Between April and June, Professor Damodaran sharpened and updated the valuation: he confirmed much of it and shifted more of its weight onto AI, doubling the AI revenue target. Through both passes, this one input stayed at zero. The model values the company at $1.25 to $1.35 trillion, with the offering at 138 percent of that. He asked his readers to check the numbers. We checked the one left at zero.

Whence the cash. Still open.

Part of a continuing read of the SpaceX offering documents, taken one at a time and in a single currency. The earlier notes totaled the disclosed cash requirement against the raise, read the two compute contracts against their terms, and tested the AI revenue assumption. This one checks the input the leading valuation leaves at zero.

On the comparison set: it is drawn from young, cash-using companies going public, the cohort that matches SpaceX. Professor Damodaran’s pre-IPO valuations since (Instacart, which had turned profitable on its advertising revenue, and Birkenstock, long profitable, both in 2023) were of cash-generating businesses, a different case.