SpaceX, Adding It Up: Reconsidering the $235 Billion Cash Gap

Regardless of assumptions, the cash gap remains an open item.

Three weeks ago we put SpaceX’s disclosed commitments into a single currency — cash — and found that the IPO would cover a fraction of what the company has said it intends to spend. The prospectus has since been priced. Two amendments have been filed, the leading valuations have published, and as of this morning another contract has been signed. We know a great deal more than we did. Every new fact has moved the picture; none has answered the question the analysis was built around. This is an update. The gap is narrower in one place, wider in others, and still nowhere aggregated.

The contract filed this afternoon

On June 5, 2026, the afternoon this was published, SpaceX filed a free writing prospectus under Rule 433. It confirmed the June 3 pricing amendment and disclosed something new: a Cloud Service Agreement signed that day with Google LLC. Google agreed to pay $920 million a month, from October 2026 through June 2029, for access to roughly 110,000 NVIDIA GPUs and supporting infrastructure — about $30.4 billion over the term. Capacity ramps through September at a reduced fee. If SpaceX fails to deliver the committed GPUs by September 30, 2026, then after a one-month grace period Google may terminate, or take fewer chips at a lower fee. After December 31, 2026, either party may leave on ninety days’ notice. Google keeps its own models and data.

To earn the first dollar in October, the capacity has to exist by September 30 — 110,000 GPUs, standing and running, four months from now. That is capital deployed now, against revenue collected monthly, later, under a contract the customer can cancel. The contract sets out the revenue. The capital to build the capacity behind it appears nowhere. One filing, the whole question.

A narrower question

Set aside the familiar objections — that SpaceX loses money, burns cash, trades at a high multiple of revenue. They are weak against a young company, and they have been answered. The question here is narrower, and it turns on amounts and dates. Allow the company its growth and the valuation, any of the published ones, at their most generous: the cash the disclosed plan requires, on the schedule the disclosures set, still runs past what the offering provides. What would close the difference is disclosed as a possibility, in a single sentence.

We estimated, then; we now estimate

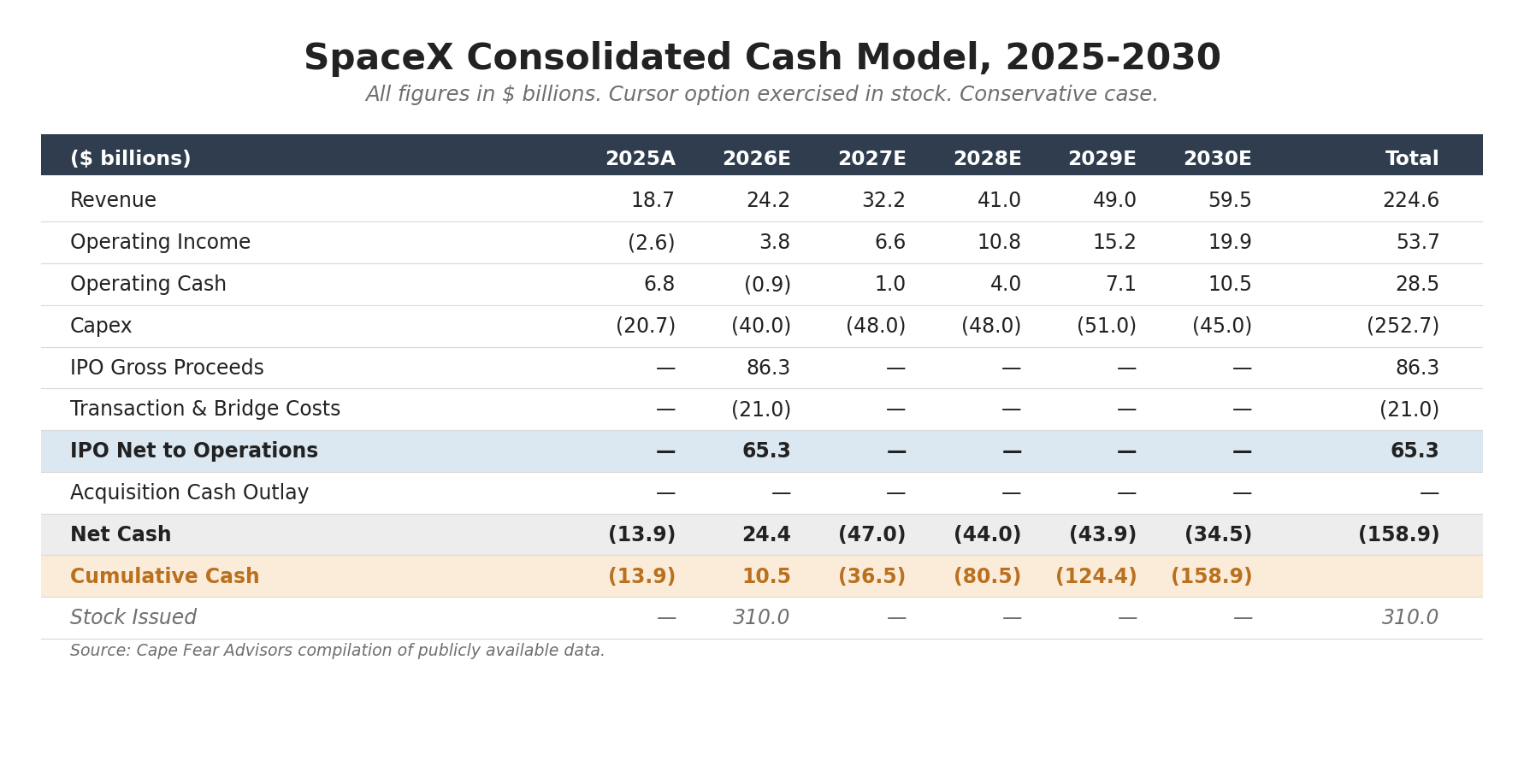

On May 10 we built a consolidated cash model for 2025 through 2030. Its headline was a cumulative shortfall near $165 billion, against an IPO then expected to net the company roughly $50 billion. Most of that model was estimate. It is now, in large part, record.

The 2025 column has been replaced with the company’s own numbers. Revenue came in at $18.7 billion, not the $15 billion estimated. Operating cash flow was $6.8 billion, which the filing attributes largely to Starlink subscriptions billed in advance. Capital expenditure was $20.7 billion, against a $15 billion estimate. Free cash flow, operating cash less capex, was negative $13.9 billion — within a tenth of a billion of the 2025 free cash flow Goldman Sachs is reported to carry. A subtraction anyone can run off the cash-flow statement and the lead underwriter’s own model reach the same figure by separate routes. The proxy and the bank agree.

The IPO line firmed, and in the company’s favor. Priced at $135, with the over-allotment, the offering grosses about $86 billion. The underwriters — Goldman, Morgan Stanley, and three others — agreed to a fee under 0.75%, a few hundred million on the largest IPO ever attempted. After the fee and the contractually required repayment of the $20 billion bridge loan, about $65 billion reaches operations. Add the cash already on the balance sheet and the company has roughly $89 billion to work with.

The first quarter of 2026 is in the filing as well. Consolidated capital expenditure was $10.1 billion in three months, $7.7 billion of it in the AI segment alone. At that quarterly pace the model’s later years look conservative, though a single quarter is thin evidence for a trend.

Update only what is now known — the actual 2025, the firmed offering — and the model’s cumulative gap is about $159 billion. It came down from the May estimate, because the raise firmed larger than expected. And it is still $159 billion: roughly twice the largest initial public offering ever priced. After that offering.

These are different measures. The $235 billion of the earlier piece was the sum of the commitments themselves — what must be spent. The $159 billion here is the cumulative cash position the model projects after the offering and after operations — what is left unfunded.

The valuations, low to high

Since May the major valuations have published, and they span more than a trillion dollars. Morningstar, the most bearish, puts fair value at $780 billion — under half the offering price — and rests the case on the AI business and the governance, not on the cash. Aswath Damodaran, the most-cited independent valuation, arrives at $1.25 to $1.35 trillion — below the price, which his own spreadsheet marks at 138% of his value. The underwriters reach higher. Morgan Stanley, a co-lead, reportedly models $330 billion of revenue by 2030 and $3.4 trillion by 2040. Goldman, the lead, projects $474 billion of revenue by 2030, with negative free cash flow every year through 2030 and the first positive year in 2031.

The numbers disagree by more than a trillion dollars. On one point they are identical. Each values the business; none sizes the cash required to build it. Goldman’s coverage goes furthest: it carries negative free cash flow every year through 2030 and names “future equity raises,” without quantifying them. The valuation is the aspiration, and the aspiration lives in the addressable market: $28 trillion in the prospectus, $26 trillion of it AI, a figure Damodaran himself says “borders on fantasy.” The larger the market assumed, the more capacity the company must build to reach it, and the more cash that build requires. The valuation and the cash requirement are the same quantity, seen from two ends.

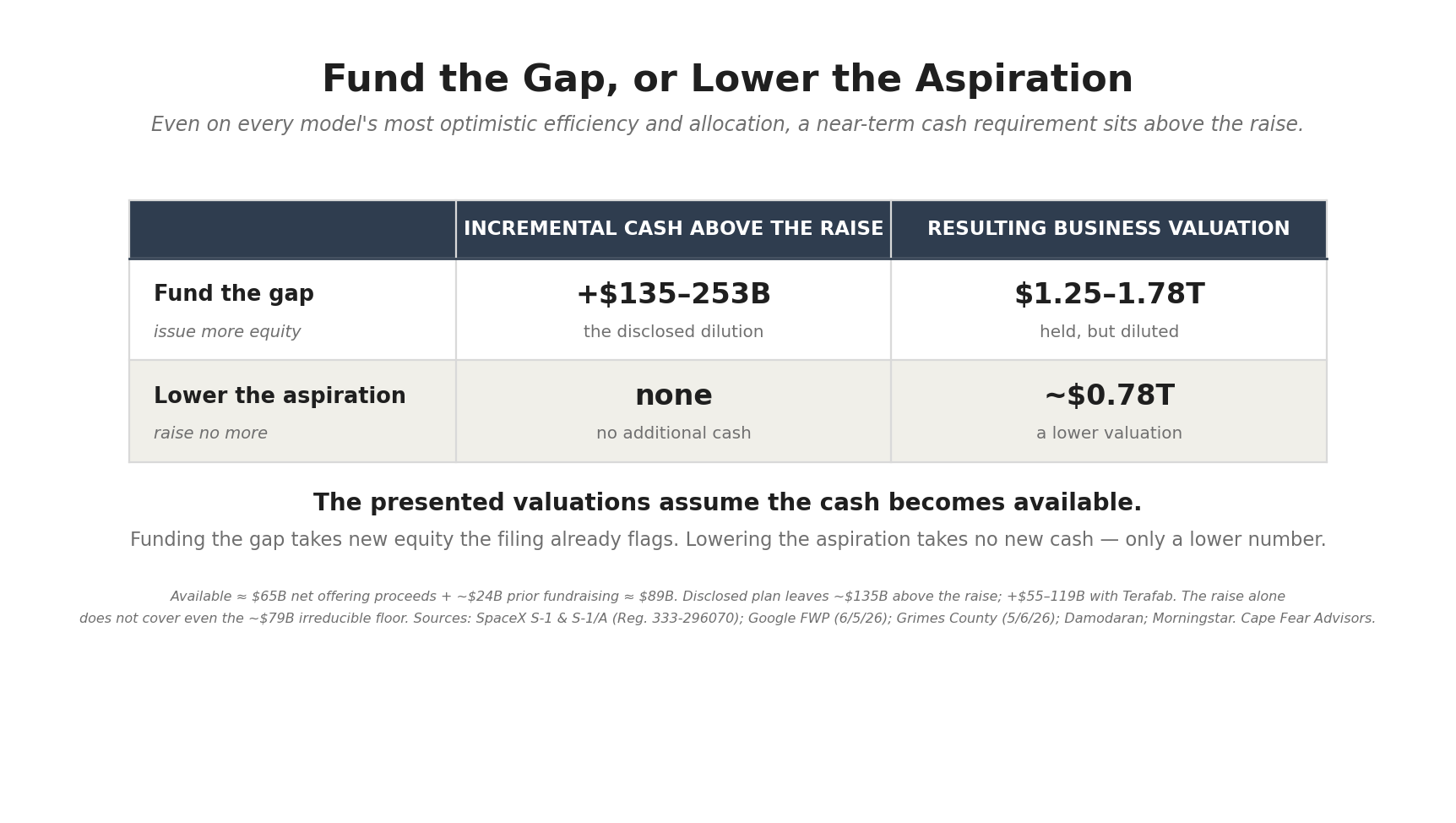

Fund the gap, or lower the aspiration

Here is the trade, on the most favorable assumptions.

To hold the aspiration — the trillion-and-a-quarter-to-1.8-trillion business — the company has to build what the revenue assumes: the Colossus II capacity behind the Google and Anthropic contracts, the Starlink and Starship deployment, and, if it is built, Terafab. The chip plant alone is $55 to $119 billion. The S-1 disavows any commitment to it — “neither Tesla nor Intel are obligated to remain a part of the project,” an obligation that runs both ways — even as, on June 3, the day the offering firmed, Grimes County approved a 100% tax abatement for the plant, against SpaceX’s pledge of a $5 billion minimum investment and 1,800 jobs.

On the cheapest version, by our model, the disclosed plan still ends 2030 about $135 billion short of the offering plus the cash on hand; build the plant and it runs toward a quarter-trillion. The difference comes from new equity, which dilutes — and it would dilute from the offering price, a level the leading valuations already sit below, raising capital above the value their own work assigns before a single new share changes hands.

Decline to build it — take “not committed” at its word — and the trade reverses. No new capital is required. But the capacity is not built in time: no 110,000 GPUs for Google by September, no wafers for 2030. The contracted revenue doesn’t arrive, and the business that remains is smaller than the published valuations assume.

There is no third cell. Nothing pairs a high valuation with a low cash requirement, because the valuation is a claim about a business large enough to need the cash. Fund the gap, or lower the aspiration. The published valuations assume the first and price neither.

Where the cash comes from

It is a fair question to ask of any cash-burning company, and the honest answer is the one everyone has already given: more will be needed, and more will be available. The market has funded SpaceX privately for twenty years. In 2025 the company raised $26.35 billion through financing activities — roughly $16 billion of AI-segment borrowing, the balance from stock sales — to cover a year in which it spent $20.7 billion against $6.8 billion of operating cash. That figure comes from the cash-flow statement itself. The access is real, and the assumption that it continues is reasonable on its face.

It is the scale that changes the arithmetic. Damodaran’s model implies an outside-capital need near $13 billion — the cumulative trough his cash flows fall into before they turn, which the IPO covers several times over — with the probability of failure set to zero. His text, separately, names overreach in AI and “tens of billions more in capital expenditures” as his chief concern. At $13 billion the cash assumption is invisible. At $135 billion and up it becomes the question, because a raise that size can be reflexive: it would come before the revenue, and large pre-revenue raises can pull the price down as they go.

The customers did not finance it. A customer that wanted the capacity could have prepaid, or taken equity to fund the build — a common structure. Google did neither; it pays monthly, in arrears, at a reduced rate during the ramp, and it can leave after December. Anthropic, the same. The two anchor customers, together about $26 billion a year, financed none of the construction. The build is SpaceX’s to carry.

The prospectus addresses its own liquidity in the conventional way. It vouches for “at least the next twelve months,” and it names the two doors without sizing either: it may “reduce future capital expenditures in this segment and reallocate,” or it may “raise additional capital or seek alternative financing sources.” Twelve months, and a choice. The horizon every valuation runs on is five years and more.

Adding it up

That is the whole of it. Choose your valuation, from Morningstar’s $780 billion to the underwriters’ multiples of it. Choose your assumptions about efficiency, about access to the capital markets, about the size of the market. Even at the company’s own stated positions, a near-term cash requirement remains that the offering does not meet. The model does only the arithmetic the filings invite, and stops there.

The requirement is disclosed, but not quantified. What that leaves is the follow-on question — from where — answered only by the language added in the amendment, as the closing line of the risk factor on integrating acquisitions, the paragraph that names xAI, the spectrum, Terafab, and Cursor:

“We may issue a significant amount of equity in connection with future transactions.”

It is the entire disclosure of the largest unfunded requirement in the document. The transactions it would fund are, by the same filing, already signed. Everyone added it up — the company, its bankers, its analysts — and the disclosure that resulted is that one sentence, which in this disclosure environment may be all that is required.

Whence the cash. Still open.