SpaceX, Adding It Up: Cursor Stock and Investment-Grade Refinancing

Another week of filings, and a shorter list of cash sources

The earlier notes in this series totaled SpaceX’s disclosed cash requirement against the money the IPO would raise, and found the raise short. This is the next update. In the week after the offering, the company signed a $60 billion acquisition in stock, earned investment-grade ratings from all three agencies, and arranged its first bond. Each was reported as a milestone. The cash requirement is where it was. The rating agencies, in their own words, say so.

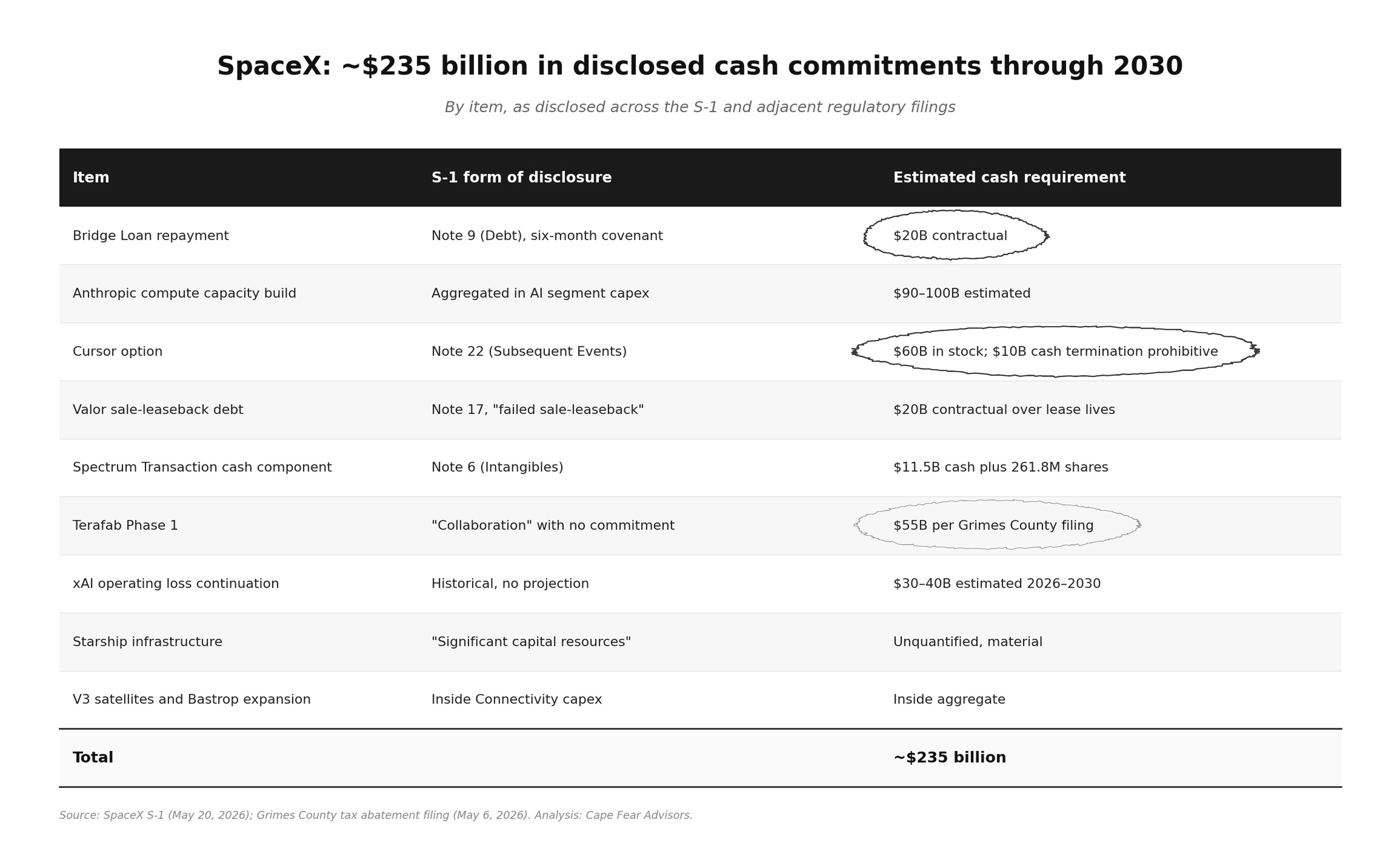

On June 16, SpaceX filed a Form 8-K converting its April option over Anysphere, the company behind Cursor, into a binding merger agreement. The deal is signed, in stock: an implied equity value of $60 billion, paid in SpaceX Class A shares, with the exchange ratio set by the volume-weighted average price over the seven trading days before closing. The option had set the choice as $60 billion in stock or a $10 billion cash payment to walk away. The merger takes the stock, and closes in the third quarter.

The form is the point. The consideration is shares, valued at the close, so the number issued floats with the price: the higher the stock trades into closing, the fewer shares change hands. It is the first use of the new public equity as currency, and the prospectus had named it. The risk factor on integrating acquisitions reserved the right to issue a significant amount of equity in connection with future transactions, and six days after the shares began trading, that sentence was a $60 billion deal. The business it brings is, by its own reporting, fast-growing and not yet profitable, its revenue consumed by the cost of the compute it runs on. That compute is bought today from other AI companies; brought in-house, it adds to the build SpaceX must fund. Either way the cash question holds. The acquisition is settled in equity, and the cash requirement stands where it stood.

On June 18, all three agencies rated SpaceX investment grade: Moody’s at Baa1, Fitch at BBB+, S&P at BBB, each with a stable outlook, all at the lower end of the scale. The agencies were specific about the basis. Moody’s rated the company under its telecommunications methodology, because Starlink carries the majority of revenue and earnings, and named Starlink the principal source of cash. The rating, Moody’s wrote, is limited by the large-scale AI buildout: its high capital intensity, persistent negative free cash flow, and an unpredictable range of returns.

The other two spoke to the cash directly. S&P projected negative free cash flow through 2029 and wrote that the company will need to raise additional capital through debt and equity markets to cover the deficits, the IPO proceeds financing part of the shortfall. Fitch put a condition on the rating: it expects the company to defer discretionary capital deployment if access to capital were limited. All three described the negative free cash flow as elective growth investment rather than a structural weakness. They rated the buildout as something the company can choose to slow.

That is the rating in the agencies’ own terms. It rests on Starlink as the cash engine, names the buildout as the constraint, and expects the company to keep raising and to slow the build if it cannot. The grade affirms the cash requirement rather than meeting it. It is given on the expectation that the requirement keeps being met, and on the company’s room to step back from the build if it is not.

The rating came at a price the company set itself, and it is paid in cash. In its filings SpaceX committed to hold a minimum cash balance of $25 billion, and the agencies credited that commitment as supporting the rating; the bridge loan’s covenant already counts unrestricted cash against the leverage limit. So $25 billion of the company’s cash is now spoken for, committed to the balance sheet to hold the grade, and held back from the buildout. The rating that lowers the cost of borrowing is the rating that freezes the cash. Following the money, that is the week’s largest movement: not cash raised, but cash immobilized.

On the same day, SpaceX’s bankers began arranging the company’s first investment-grade dollar bond, expected the following week, at a size reported as at least $20 billion and not yet fixed. The bond is required. The bridge loan SpaceX took in March, after acquiring xAI, matures September 2, 2027, and the prospectus obliges the company to apply IPO proceeds to repay it within six months of the offering. The bond refinances that bridge, new debt for old, and settles a maturity already on the clock. It leaves the cash requirement where it stood. Should the bond price above the amount the bridge needs, the excess would add to available cash, at a spread that is next week’s figure.

So the week set down three documents. The acquisition is signed, in stock. The ratings are investment grade, resting on Starlink, naming the build as the constraint and the raising as the expectation, and carrying the $25 billion the company has committed to keep idle. The bond refinances a bridge already due. The two figures the week put in play are circled above: the $60 billion settled in stock, and the $20 billion refinanced in debt. Both went to other ends; the buildout drew on neither.

Whence the cash. Still open, and now with fewer ways to answer.

— — —

Part of a continuing read of the SpaceX offering documents, taken one at a time and in a single currency. Sources: SpaceX Form 8-K, June 16, 2026 (Anysphere merger agreement); Moody’s, Fitch, and S&P rating actions, June 18, 2026; SpaceX Form S-1 and the SpaceX Bridge Loan credit agreement; press reporting on the bond offering. Figures verified against the primary filings. Analysis: Cape Fear Advisors.

Appreciate your work, thank you!