CoreWeave, Adding It Up

A Cash Reconstruction Exercise

CoreWeave’s financial statements are accurate, its auditor’s opinion is clean, and there is no going-concern question. Read from the income statement, at the assumptions the company applies, the business is approaching profitability. Read from the cash flow statement taken whole, the reported operating cash is in net the money customers paid in advance, the cash spent on the fleet runs well ahead of the cash earned delivering compute, and the gap is funded externally every year. Both readings are accurate. Between them sit a handful of accounting judgments the company discloses and the reader is left to resolve, two of them flagged by its own auditor as the hardest in the audit. One calculation determines which reading is the more illuminating one for an analysis, and the filings hold every input to it. This piece lays out the judgments and arrives at that calculation: whether a unit of compute is sold for more than it costs to deliver.

Serious people are raising questions about what’s happening at CoreWeave, and because it matters to our other work, we paused to take a look. The questions in the air are good ones. Whether the depreciation schedule runs too long. Whether the debt is too heavy. Whether the customer contracts are as solid as the backlog suggests. Whether the whole thing is a bubble. There is an instinct underneath them that something might be wrong. Read the filings for a concealed flaw and they come back clean. What is worth seeing here is in plain sight.

So we read them for something else, the same thing we read the SpaceX filings for. The interesting feature of these companies is the disclosed architecture: what the documents are built to show, and where what they show leads. With SpaceX it led to one question the filings invite and the reader has to answer alone, which was where the cash comes from. With CoreWeave it leads to a calculation the filings supply every input for and leave to the reader to run. This matters now beyond CoreWeave, because the same structure is about to be tested again by Anthropic and by OpenAI when their numbers reach a filing, and CoreWeave is the cleanest case to learn to read it on. It is already public, already audited, already rated.

So our question is narrower than the ones in the air. Set aside whether the schedule is too long, the debt too heavy, the moment a bubble. Ask instead whether a unit of compute earns more than it costs to deliver. Everything below is the company’s own disclosure, arranged until that question comes into view.

A note before the numbers, because it is the whole posture. This reconstruction relies on the figures. CoreWeave disclosed material weaknesses in internal control over financial reporting, of the kind common for a recently public company, and stated that the deficiencies did not result in a material misstatement. The auditor issued an unqualified opinion. The statements carry no going-concern qualification. We take all of it as given, and depend on it.

The numbers the company reports

For the quarter ended March 31, 2026 (Form 10-Q): revenue of $2,078 million; cost of revenue $716 million, covering facilities, rent, power, and depreciation of power installations; technology and infrastructure of $1,273 million, which the company describes as the depreciation and amortization on its servers, switches, networking equipment and software, together with research-and-development staff; sales and marketing $69 million; general and administrative $164 million; an operating loss of $144 million and a net loss of $740 million. Interest expense, net, was $536 million, with a further $97 million capitalized. Depreciation and amortization was $1.1 billion.

Property and equipment, gross, was $40,933 million, of which technology equipment is $26,627 million and construction in progress, which neither depreciates nor yet earns, is $9,581 million.

At December 31, 2025 (Form 10-K) the company ran 43 data centers with over 850 MW of active power and roughly 3.1 GW of total contracted power to deploy over future periods. It does not disclose how many GPUs it operates. It discloses the architecture: NVIDIA GB200 and GB300 NVL72 systems.

What the contracts are, and what that decides

The first judgment is whether CoreWeave sells a service or leases equipment, and the auditor, Deloitte & Touche, named it a Critical Audit Matter, defined in the opinion as a matter material to the statements that involved “especially challenging, subjective, or complex judgments.” In Deloitte’s words the significant judgments include determining “whether the contracts with customers are accounted for as a revenue contract for cloud-based services or a lease contract for cloud computing equipment, and the identification and treatment of contract terms that may impact the timing and amount” of revenue. The company concluded service, not lease: because “generally either there are no identified assets or customers do not control or direct the use of underlying hardware,” the arrangements are accounted for as service contracts under ASC 606.

That conclusion carries consequences through the statements. It keeps the GPUs on CoreWeave’s books as its own assets, depreciated by CoreWeave, with the depreciation reported in technology and infrastructure, below the gross-margin line, rather than in cost of revenue. The reported gross margin therefore does not carry the depreciation of the equipment that earned the revenue.

It also builds the collateral. Because the contracts are services and the GPUs are CoreWeave’s, both the equipment and the contracted revenue stay on CoreWeave’s side of the ledger, and both are then pledged for the debt that bought the equipment. The company describes its delayed-draw term loan facilities, $11.8 billion outstanding, as “collateralized with the assets underlying the contributed contracts and the pledged contractual cash flows, generally from investment grade counterparties,” amortizing “as contracted cash flows are generated.” The facilities run through named CoreWeave subsidiaries, CoreWeave Compute Acquisition Co. VIII, LLC among them, secured by first-priority pledges of those subsidiaries’ equity and assets, non-recourse. The subsidiaries are consolidated; the assets and debt stay on the balance sheet. So the GPUs and contracts the service judgment leaves on CoreWeave’s books are the same GPUs and contracts that secure the debt. The question this reconstruction reaches, whether a unit’s revenue covers its cost over the asset’s life, is a question about the very assets and revenue pledged as collateral.

Six years, or five

The company depreciates technology equipment over six years. Effective January 1, 2023 it changed that estimate from five years to six, citing “continuous advancements in hardware performance, software optimization, and data center design improvements,” and disclosed the effect: $20 million less expense and $0.10 more earnings per share in 2023. Over the same span the equipment’s supplier, NVIDIA, has described annual architecture generations, Hopper, Blackwell, Rubin, and stated generational efficiency gains of up to 25 times. The accounting life spans six of those generations.

The estimate is the company’s to make, and this reconstruction does not substitute its own. It records one property of it. The estimate changes reported operating income and does not change cash, because depreciation is non-cash. A longer life lowers the reported charge and lifts reported income; the cash is identical. The income statement’s profitability moves with the assumption. The cash does not.

The cash, read whole

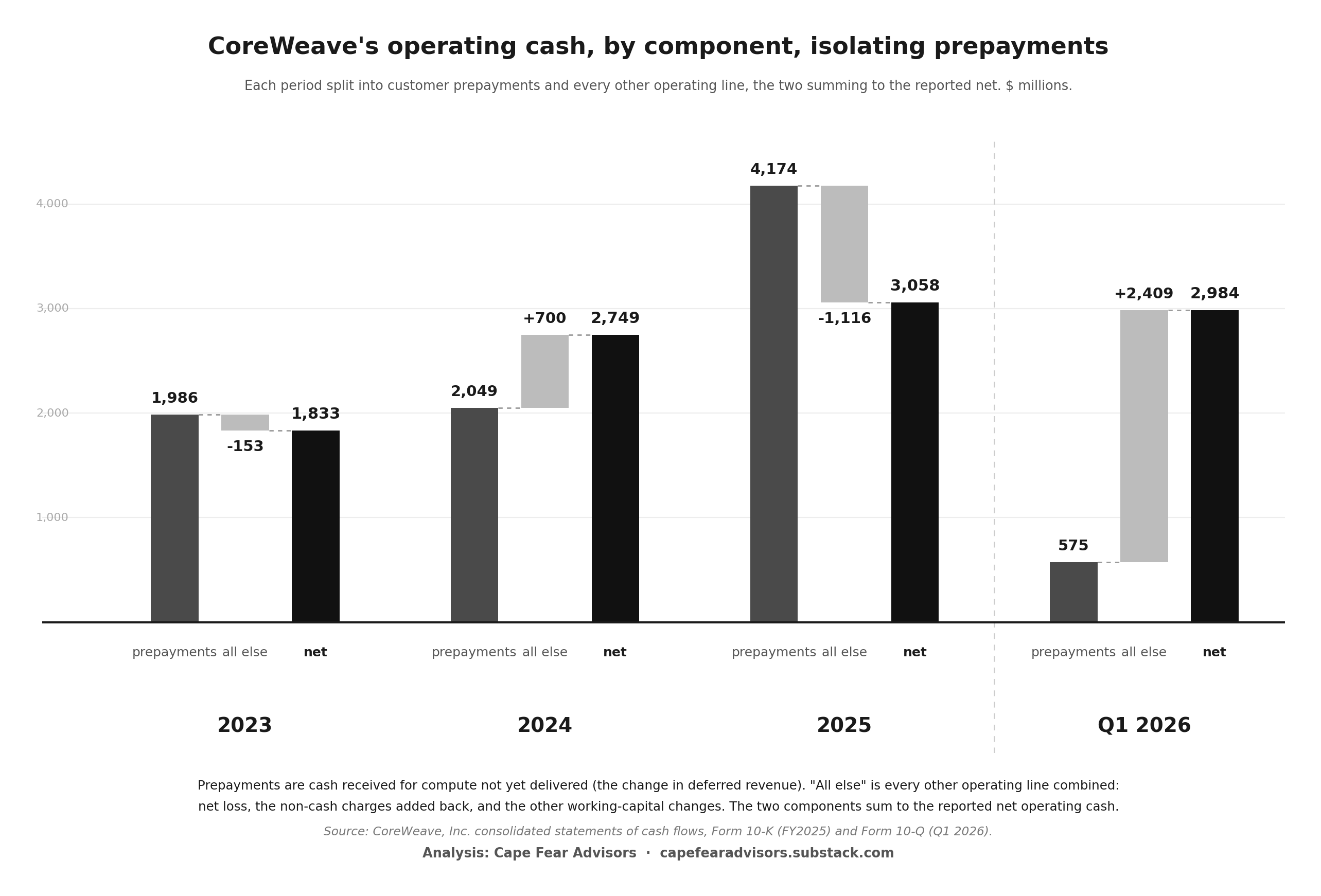

Start with what the company reports. Operating cash was positive and rising across three years: $1,833 million in 2023, $2,749 million in 2024, $3,058 million in 2025. This is the figure the growth reading rests on, a business whose operations throw off cash, with capital spending building future capacity.

Inside that operating cash sits the prepayment. Customers pay in advance, and the cash arrives in operating activities as the deferred-revenue line: $1,986 million in 2023, $2,049 million in 2024, $4,174 million in 2025. This is an ordinary part of operating cash, recorded as the accounting requires. It is worth isolating not because it is unusual but because of what it is: cash received for compute not yet delivered, the customer financing the very service whose economics are the question here. Set it beside the operating cash. In 2023 the prepayment inflow was larger than the operating cash; in 2024 it was most of it; in 2025 it was larger again, $4,174 million against $3,058 million. Remove the prepayment from each year and the operating cash reads $(153) million in 2023, $700 million in 2024, and $(1,116) million in 2025. Across the three full years, the reported operating cash is, in net, the cash customers paid ahead of delivery, cash recorded against compute owed later, on fleet in part still to be bought.

The first quarter of 2026 reads differently. Operating cash was $2,984 million; the prepayment inflow that quarter was $575 million, a smaller share. Remove it and operating cash is still positive, about $2,409 million. The quarter rested instead on two other movements: accounts receivable came in, a $1,042 million collection, and accounts payable and accrued expenses rose, a $960 million inflow from paying vendors more slowly. A single quarter turns on whichever working-capital line happens to move; the three-year pattern is the steadier fact, and the prepayment is one working-capital line among several. The full set of them, for the quarter, is in the next section.

Against that operating cash, the fleet. Cash spent on property and equipment was $7,695 million in the quarter ended March 31, 2026, and $10,271 million across 2025. The cash earned and the cash spent on the fleet are the same compute, entered in two sections of the one statement. The investing figure runs growth and replacement together: the capacity not yet earning, and the fleet consumed earning current revenue. The split between them is where the two readings of the business diverge, and the filing carries the combined figure. The reader who wants the split assembles it.

The three years hold one shape. Operating cash positive, and made of prepayment. Investing cash larger and negative: $(3,148) million, $(8,658) million, $(10,271) million. Financing cash filling the gap each year: $1,788 million, $7,464 million, $9,308 million. The cash spent on the fleet runs ahead of the cash earned from delivering compute, and the difference is raised, every year shown, from customers paying in advance and from capital markets.

What has been paid for, and when it comes due

This would be an accounting curiosity but for what the company has already been paid. Customer prepayments, recorded as deferred revenue, were $7.5 billion. Deferred revenue is an obligation to deliver compute, measured at the cash received for it. The cash has been spent, on the fleet, in the investing line above. The obligation to deliver remains.

Remaining performance obligations were $98.8 billion, of which the company discloses 36% converts in months one through 24, 39% in months 25 through 48, and the rest in months 49 through 84. Sixty-four percent lands in year three and beyond: compute contracted, and in part prepaid, now, to be delivered across a horizon that runs well past the current equipment, on fleet not yet acquired, whose acquisition the cash the business generates has not so far funded without external capital.

The obligation is also concentrated. For the quarter, one customer was 45% of revenue and a second was 20%. A year earlier the first customer alone was 72%. The contracted revenue that secures the debt and underwrites the backlog is, by the company’s own disclosure, drawn substantially from one customer, then two.

The change in deferred revenue during the quarter was, in the company’s words, “primarily driven by reclassification of $1.3 billion to customer liabilities.” Total deferred revenue fell from $8.2 billion to $7.5 billion over the quarter; the $1.3 billion left the deferred-revenue line, much of it non-current, and appears in other current liabilities, which rose from $162 million to $1,534 million. No cash moved. What changed is the obligation’s classification, out of deferred revenue, which is discharged by delivering compute, and into a current customer liability, a nearer-dated obligation of a form the filing does not state. The filing does not give the cause, and this piece does not supply one.

In the same quarter, the other side of the customer relationship moved too. Accounts receivable fell from $3,169 million to $2,120 million, a $1,042 million collection that arrives in operating cash as an inflow. So within one quarter the company collected down a billion dollars of what customers owed it, took on $1,748 million more owed to its vendors, with accounts payable rising from $1,623 million to $3,371 million, and reclassified $1.3 billion of what it owed customers from a promise of compute into a current liability. Each of these adds to reported operating cash, and each is the timing of who pays whom and when. The filing records the movements and leaves them there.

On the balance sheet, and beside it

The company’s debt was $25,149 million as of the quarter-end balance sheet, at stated effective interest rates ranging from 2% to 15% across the individual facilities and notes, the lowest being a convertible note and the highest a delayed-draw term loan. Against that it held $2,244 million in cash, plus $777 million restricted. After the quarter closed it raised more, on top of that balance and in the same pattern: $4.0 billion of 1.75% convertible senior notes in April 2026, disclosed as a subsequent event; and in June 2026 it priced $1.25 billion of 9.625% senior notes and €2 billion of 8.500% senior notes, both due 2032, a roughly $3.5 billion raise. These are senior unsecured. The lower-cost facilities, by contrast, are in the company’s description secured by cash flows “generally from investment grade counterparties.” The counterparties are investment grade, not CoreWeave, whose own corporate credit is rated below investment grade by all three major agencies, Moody’s at Ba3, S&P at B+, and Fitch at BB-. The 9.625% coupon on the June unsecured notes is the price at which that credit raised unsecured money.

Some of the structure sits beside the balance sheet rather than on it. The company discloses an unconsolidated joint venture in which a developer holds 85% and CoreWeave 15%, where CoreWeave provides construction, administrative and property management, is the anchor tenant under a 15-year lease, guarantees up to $95 million, and may have to fund the build “to the extent the JV is unable to secure third-party financing.” Whether CoreWeave is the primary beneficiary, and so must consolidate the entity, is the second Critical Audit Matter the auditor named. The company concluded it is not, and does not consolidate.

It is not the only such arrangement. The company also discloses, under DCSP Financing Arrangements, a data center service provider that will “design, purchase, build, and manage” a data center for it, in which CoreWeave is at once the customer, the lender (a senior secured loan of up to $305 million at 13%), and the seller-lessee of $116 million of infrastructure assets it “continues to control,” recorded as a financing obligation at a 15% imputed rate. And it discloses a category of leases with developer-operators it treats as unconsolidated. The same shape recurs from the other side, too: in June 2026 a subsidiary of Prime Data Centers sought roughly $850 million in bonds to fund a build leased entirely to CoreWeave for 15 years, about $2.2 billion in rent, with CoreWeave carrying substantially all operating costs. The arrangement the consolidation judgment leaves off CoreWeave’s balance sheet is, there, recorded on someone else’s.

What the auditor marked as hard

Four judgments shape how the business reads: the contract characterization, the useful life, the classification of fleet spending, and the consolidation of the financing entity. Each is the company’s to make, the company made each one, and the auditor concurred and issued an unqualified opinion. Two of the four the auditor also singled out as Critical Audit Matters, the service-versus-lease characterization and whether to consolidate the joint venture, a designation reserved by the standard for matters that were material to the statements and involved especially challenging, subjective, or complex judgment. The independent auditor agreed with the company on both, and recorded that these two were among the hardest calls in the audit.

Each judgment carries a consequence, on the record. Treating the contracts as services keeps the equipment depreciation below the gross-margin line and keeps the assets and the contracted revenue on CoreWeave’s books, where they can be pledged. Six years rather than five lowers the annual depreciation charge and lifts reported income. Classifying the fleet spending as growth places it in investing rather than in cost of revenue. Concluding CoreWeave is not the primary beneficiary places the financing entity beside the balance sheet rather than on it. This piece sets the four down with their consequences. The reader weighs them.

The question

The company is paid, in part in advance, to deliver compute. Two-thirds of that obligation comes due in year three and beyond, from one and then two customers, on fleet still to be bought. The operating cash the business reports is in net the prepayment for that compute; the cash spent on the fleet runs ahead of the cash earned delivering it; the gap is raised each year from customers paying ahead and from capital markets.

Per-unit cost against revenue, over the life of an asset, is a calculation no company is required to publish, and its absence here is ordinary. It matters for this business because it is the calculation the answer turns on. The filings hold every input. A reader can run it.

So the question is the one the good questions circle. Set aside whether the schedule is too long, the debt too heavy, the moment a bubble. The question underneath them is whether a unit of compute is sold for more than it costs to deliver. The filings disclose everything required of them, and the calculation waits in the inputs for whoever assembles it. The machine is running. This is what it runs on.

Analysis: Cape Fear Advisors · capefearadvisors.substack.com

Sources: CoreWeave, Inc. Form 10-Q for the quarter ended March 31, 2026, and Form 10-K for the year ended December 31, 2025 (financial figures, capacity, useful-life estimate, deferred revenue, remaining performance obligations, customer concentration, debt terms, the joint venture and DCSP arrangements, and the report of independent registered public accounting firm, Deloitte & Touche LLP). April and June 2026 note offerings: CoreWeave press releases, April 14 and June 11, 2026. Corporate credit ratings (Moody’s Ba3, S&P B+, Fitch BB-): the respective agencies’ rating actions. NVIDIA architecture cadence: NVIDIA public statements, GTC 2026.